Ty J. Young, Revisited

Ty J. Young’s fine print continues to be a must-read for consumers.

Think twice before handing over your retirement nest egg to this company.

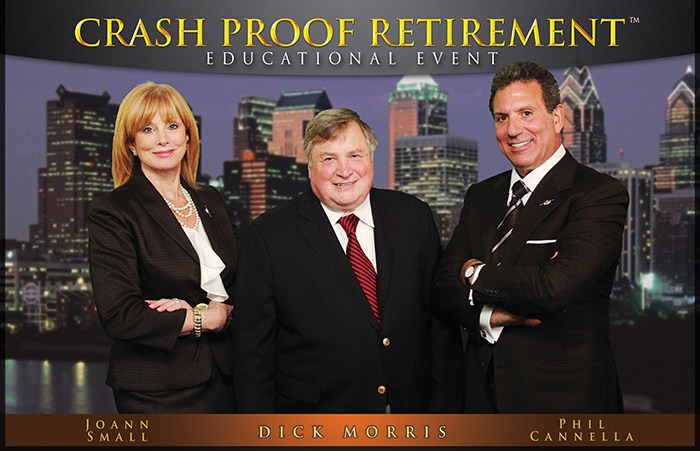

The Crash Proof Retirement System is marketed to retirees and soon-to-be retirees as a slam-dunk investment strategy that is immune to market losses.

“The market goes up, you go up; the market goes down, you stay even,” says perpetual prognosticator and former Fox News pundit Dick Morris in a recent TV commercial in which he endorses the system. “There are enough uncertainties in life,” Morris says. “Don’t let your retirement become one of them.”

Morris does not disclose the investment vehicles at the center of the system, nor for that matter does the Crash Proof Retirement website. But a TINA.org review found the system’s primary retirement products to be fixed index annuities, in which an initial premium or principal (e.g., a retirement nest egg) is paid back to a buyer plus any earnings related to the performance of a stock market index (e.g., the S&P 500) after a holding period ends.

Fixed index annuities are popular in part because principal is guaranteed; or, as Morris puts it, “the market goes down, you stay even.” But there’s more to them than that. Here’s what you should know about fixed index annuities and how the Crash Proof Retirement markets and sells them through First Senior Financial Group before heading down to one of the company’s free seminars:

Find more of our coverage on retirement here.

Our Ad Alerts are not just about false and deceptive marketing issues, but may also be about ads that, although not necessarily deceptive, should be viewed with caution. Ad Alerts can also be about single issues and may not include a comprehensive list of all marketing issues relating to the brand discussed.

Ty J. Young’s fine print continues to be a must-read for consumers.

A network marketing coach doesn’t deliver on his (expensive) promises.

Precious metals seller pulls coronavirus-related radio ad following TINA.org inquiry.