TINA.org Joins Consumer Advocates to Keep FTC Bipartisan

Why agency independence is in the best interests of consumers.

TINA.org joins coalition of consumer organizations in support of the proposed rule

| | CFPB Proposes Paycheck Advance Rule

UPDATE 11/15/24: In November 2024, the FTC sued online cash advance app Dave for misleading consumers about the amount of money they could receive and charging them fees disguised as “tips” without their consent. Our original blog follows.

There was a time when workers were paid daily at the ends of their shifts – gone are those days. Instead, 73 percent of workers wait two weeks or more for their paychecks (while employers get the benefit of keeping the money for longer stretches). For low-income employees working paycheck to paycheck, those weeks of waiting can be problematic, especially for any unexpected costs that arise.

To meet the need for fast cash, a growing number of companies are offering paycheck advance products to give workers their earned wages early. In 2022, more than 7 million workers accessed about $22 billion in earned wages through employee-sponsored paycheck advance programs, according to an analysis by the Consumer Financial Protection Bureau. Other companies offer these services directly to users.

The problem? These products are often marketed as having “no fee” or that they have “no hidden fees.” But the truth is that these products often do have a cost, especially for “expedited” access to the money – the very reason that people are using these services.

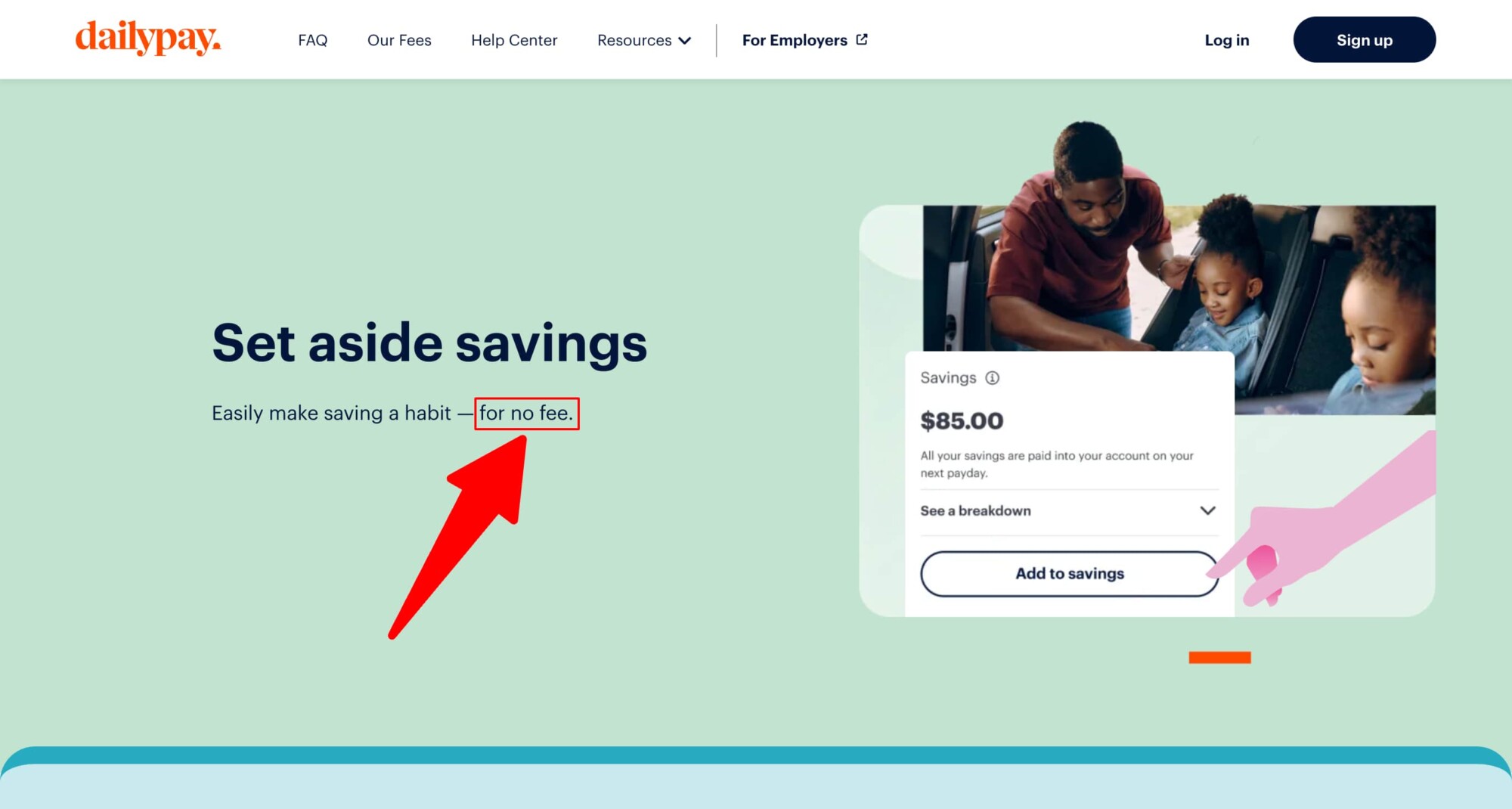

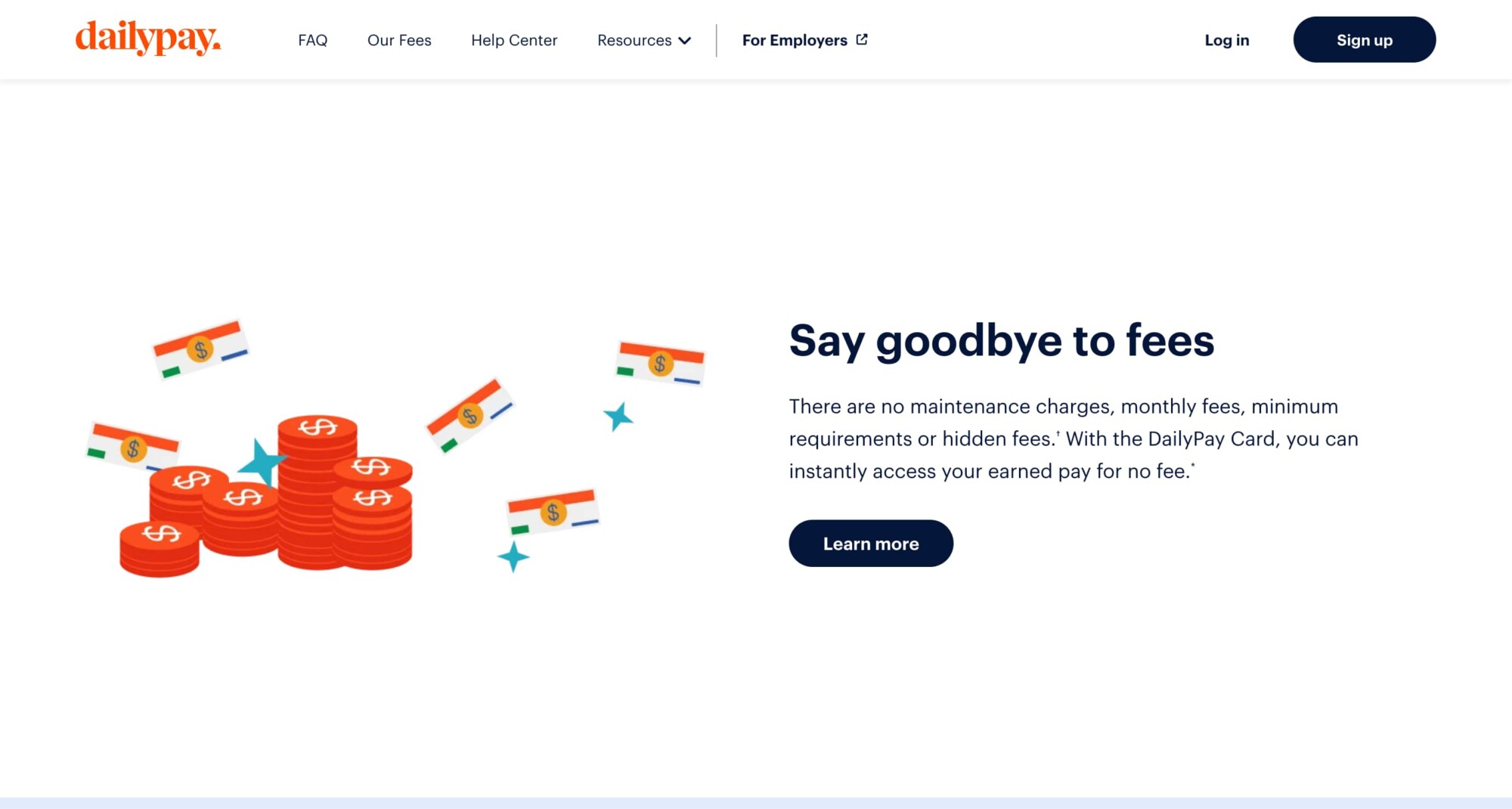

DailyPay advertises that “you can instantly access your earned pay for no fee.” But for immediate access to the wages, the company actually charges an “instant transfer fee” of $3.49.

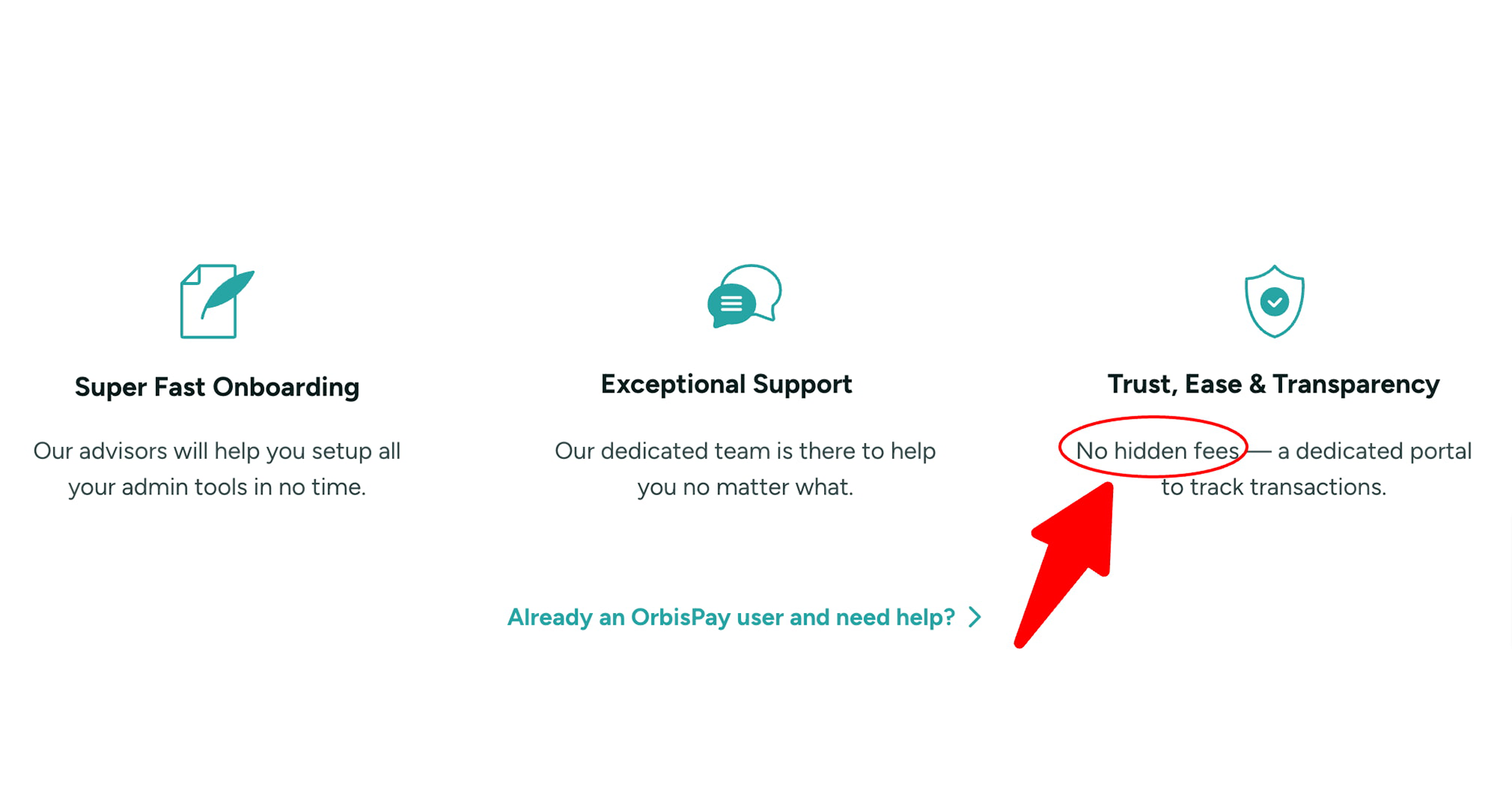

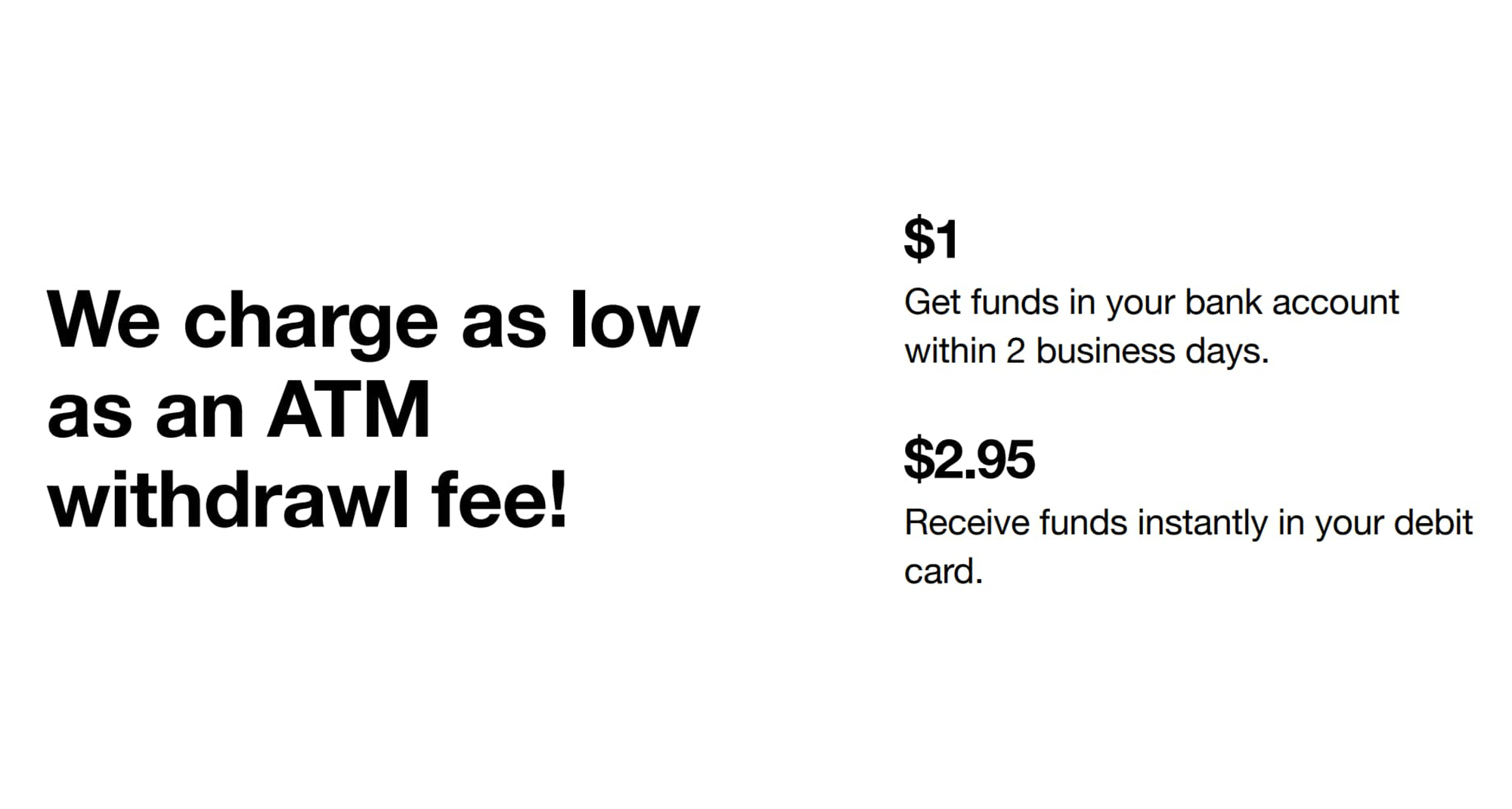

Orbispay offers “no hidden fees,” but one has to search beyond their website for the details of what the fees actually are:

Some companies even pressure consumers to “tip” them for the service (which begs the question, why is the customer tipping the bank?). When the fees are compared to the amounts of money borrowed, the cost is often equivalent to APRs of 109.5 percent on average or sometimes even as high as 498 percent or more.

This strategy pays off for the lenders. For instance, Dave reported to the SEC that it earned $62 million in tips in 2022. Using that SEC report, the CFPB determined that “a $144 transaction for a seven-day period, with $8 in fees (the combined average tip and fee amount) equates to a 290% APR.”

The California Department of Financial Protection and Innovation identified “multiple strategies that lenders use to make tips almost as certain as required fees,” including “disabling a service if a borrower does not tip,” and “setting default tips and using other user interface elements to make tipping hard to avoid.”

To address these misleading practices, the Consumer Financial Protection Bureau proposed an interpretive rule that would apply the Truth in Lending Act to these paycheck advance products. The proposal seeks to ensure that lenders are disclosing the real costs and fees to employees who are using these products.

CFPB Director Rohit Chopra remarked on the proposal: “The proposal would … help to ensure that consumers can compare options and that companies compete on clarity, not confusion. … We want to see the market compete down costs for employees and employers, rather than innovate on ways to harvest junk fees and push people into cycles of debt.”

To support the proposed rule, TINA.org signed onto a comment letter from a coalition of consumer protection organizations led by Americans for Financial Reform and which include Consumer Federation of America, Consumer Reports, National Association of Consumer Advocates, National Consumers League, and National Consumer Law Center. Among other things, the comment states that “[l]enders should not be allowed to disguise 300% APR loans in so-called ‘tips,’ expedite fees or other junk fees, or by claiming that their loans are not loans. Advances of wages or other income, repaid later, are loans regardless how they are styled. All payday advances need clear cost and fee disclosures.”

Click here to read the comment.

Why agency independence is in the best interests of consumers.

Council blesses MLM’s use of unsubstantiated earnings claims.

Legislators should protect the work of the Consumer Financial Protection Bureau.