Best Reader Tips of 2021

This year reader tips led to dozens of ad alerts, as well as a complaint to regulators.

This Thanksgiving, ensure you know what's what with the various assurances of travel insurance.

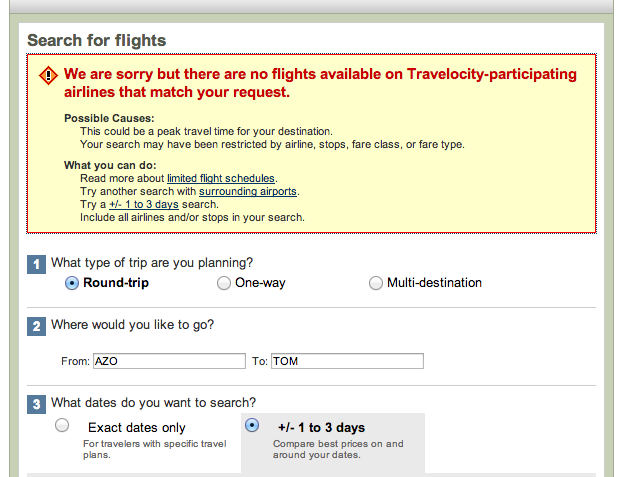

Perhaps you’re looking to book a flight from Kalamazoo to Timbuktu for vacation:

Well then you’re out of luck. (Also: Don’t go to Timbuktu right now.) But how about here to Los Angeles?

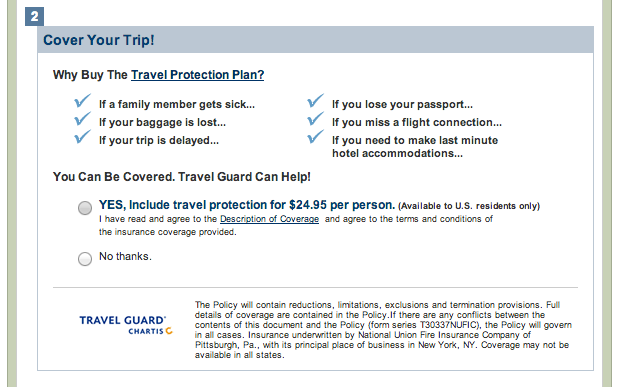

There we go. But wait – Travelocity wants to know at checkout whether you want a Travel Protection Plan.

What if Grandma gets sick and can’t fly? Flight cancellation fees are expensive, and most tickets bought through discount sites are nonrefundable. Should you pay the extra $25 per person for the protection plan?

Maybe. Discount travel sites like Travelocity, Expedia, and Orbitz often offer travel insurance and travel protection plans at checkout that claim to cover you for a variety of issues including illness, lost baggage, and delayed trips. You can also purchase travel insurance and protection plans separately for any trip you are taking. But not all coverage is the same, and you might not end up with the coverage you need. Here’s what consumers should know.

1. Make sure you’re buying insurance and not something else

Travel insurance and “travel protection” are not the same things. A travel insurance policy is sold by a regulated insurance company and has the added consumer protection of having to follow the regulations of the state where the policy is sold.

But products advertised as “travel protection” that are not provided by an insurance company could be anything. (The above example from Travelocity, though called a protection plan, is actual insurance underwritten by an insurance company.) If you need to make a claim, you might be out of luck with a protection plan. A real insurance policy underwritten by an established and financially stable insurance company provides consumers with better legal protection and more recourse to get back their money. The same safeguards don’t apply to unregulated protection plans.

2. Cover only what you need covered

Many travel insurance plans sold at checkout will cover trip delays, medical expenses incurred abroad, lost baggage, and so on.

But many consumers don’t need all that protection. Some health insurance plans cover your medical costs wherever you go. Airlines are required to compensate you for lost luggage up to $3,000 in the U.S. and $1,500 worldwide (though if your luggage is stolen at the hotel, that loss may be covered by your own travel insurance). And some credit cards provide coverage should you miss prepaid reservations during your travels due to flight delays.

To avoid paying higher premiums, check for plans that offer only what you need and do not duplicate what you already have.

3. Check the fine print

Travel insurance plans vary in scope. You should consider what you need. Are you going to a country under attack by rebels? Are you planning to have any risky adventures? Many plans won’t cover pre-existing medical conditions or delays caused by known conditions in a country. Read up on the current events in the country before you go. If the State Department has issued a travel advisory before your trip and your flight is delayed for the reasons laid out in the advisory, you likely won’t be covered for missed reservations. And if your trip ends early because you’ve been kidnapped by rebels in Timbuktu, your travel insurance isn’t going to cover your losses. (Though at that point, you’ll probably have other worries.)

4. Shop around

The travel insurance offered at checkout from discount travel sites may not be a bad deal, but there might be a better one out there. Taking the first offer isn’t always the best idea. Are you covered for everything you need with that policy? Do you understand the fine print and what the policy’s exemptions are? Is the insurer licensed? Are the exclusions excessive? These are all questions that should be answered before you click “buy.”

For more consumer pitfalls during travel, see our article on travel scams and this FTC alert.

This year reader tips led to dozens of ad alerts, as well as a complaint to regulators.

These claims may trip you up.